Physical Address

Remote team based in Bozeman, Montana.

Physical Address

Remote team based in Bozeman, Montana.

KYC/AML automation for fintech startups: comply with May 2026 EBA guidelines, cut costs 80%, and onboard customers in minutes. Compare top 5 platforms and implementation roadmap.

Why KYC/AML Automation Is Critical for Fintech Startups in 2026

KYC/AML automation for fintech startups is no longer optional. It is a survival requirement.

In May 2026, the regulatory landscape has fundamentally shifted. The European Banking Authority (EBA) has begun actively enforcing new guidelines on the use of remote customer onboarding solutions under PSD2 and AML/CFP directives. Fintech startups that fail to implement automated solutions face existential risk.

KYC/AML automation for fintech startups solves the impossible equation facing every financial technology founder: how to onboard customers quickly while preventing money laundering.

| Regulation | Effective Date | Impact on Fintech Startups |

|---|---|---|

| EBA Remote Onboarding Guidelines | May 2026 | Strict video identification and document verification standards |

| AMLD6 Implementation | June 2026 | Expanded criminal liability for compliance failures |

| SEC Rule 13f-2 | May 2026 | Large short position reporting requirements |

| Beneficial Ownership Registry | January 2026 | Centralized database of company owners |

KYC-AML automation for fintech startups helps you meet these requirements without hiring a team of 20 compliance officers.

| Consequence | Typical Impact on Startup |

|---|---|

| Regulatory fine | 50,000−10,000,000 |

| Forced shutdown | Immediate business cessation |

| Founder liability | Personal criminal charges |

| Banking relationship termination | Loss of payment processing |

| Reputational damage | Permanent customer loss |

KYC/AML automation for fintech startups is not a cost center. It is risk insurance.

For related compliance guidance, see Fintech Compliance 101: What Small Businesses Need to Know.

KYC/AML automation for fintech startups refers to software platforms that use artificial intelligence, machine learning, and API integrations to automatically verify customer identities, screen against watchlists, monitor transactions, and file regulatory reports.

| Pillar | What It Automates | Manual Alternative |

|---|---|---|

| Customer Identification | ID document verification, biometric matching, liveness detection | Staff manually reviewing passport photos |

| Watchlist Screening | Sanctions, PEP, adverse media checks against global databases | Manual searches on multiple government websites |

| Transaction Monitoring | Real-time scanning for suspicious patterns | Spreadsheet tracking (impossible at scale) |

| Reporting | SAR, CTR, and other regulatory filing | Manual form completion and mailing |

KYC/AML automation for fintech startups handles all four pillars without human intervention.

| Metric | Manual KYC/AML | Automated KYC/AML |

|---|---|---|

| Customer onboarding time | 3-7 days | 2-5 minutes |

| Cost per verification | $50-150 | $1-5 |

| False positive rate | 15-25% | 2-8% |

| Staff hours per week | 40-100+ | 5-10 |

| Scalability | Linear (hire more) | Exponential (add volume) |

KYC/AML automation for fintech startups delivers these improvements simultaneously.

For automated tax solutions, see Automated Tax Filing for Digital Nomads.

Understanding the true cost of manual compliance helps justify KYC/AML automation for fintech startups.

| Expense Category | Manual Cost (Startup) | Automated Cost |

|---|---|---|

| Compliance staff (2-3 people) | 120,000−240,000/year | $0 (automated) |

| Per-verification cost | $50-150 | $1-5 |

| Database subscriptions | 10,000−50,000/year | Included in automation |

| Audit preparation | 20,000−100,000/year | 5,000−20,000/year |

| Regulatory filing fees | 5,000−50,000/year | 5,000−50,000/year |

| Total Annual Cost | 180,000−180,000−500,000+ | 10,000−10,000−75,000 |

| Hidden Cost | Impact |

|---|---|

| Lost customers due to slow onboarding | 30-50% abandonment rate |

| Employee burnout and turnover | $50,000+ per departure |

| Missed fraud leading to fines | 100,000−10,000,000 |

| Competitive disadvantage | Customers choose faster competitors |

| Scaling limitations | Cannot grow beyond manual capacity |

KYC/AML automation for fintech startups eliminates both direct and hidden costs.

When evaluating KYC/AML automation for fintech startups, look for these essential features.

| Feature | Why It Matters |

|---|---|

| ID document verification | Accepts passports, driver’s licenses, national IDs from 150+ countries |

| Biometric liveness detection | Prevents deepfake and photo spoofing attacks |

| Global watchlist screening | Sanctions, PEP, adverse media from 1,000+ sources |

| Ongoing monitoring | Continuous screening, not just at onboarding |

| Transaction monitoring | Real-time detection of suspicious patterns |

| Case management | Dashboard for reviewing flagged customers |

| Audit trail | Complete record of all compliance decisions |

KYC/AML automation for fintech startups must include all core features to be viable.

| Feature | Why It Matters |

|---|---|

| AI-powered risk scoring | Predicts customer risk level automatically |

| Behavioral biometrics | Detects account takeover via typing patterns |

| Blockchain analytics | Traces crypto transaction origins |

| Automated SAR filing | Submits reports to regulators directly |

| No-code workflow builder | Customize rules without engineering |

| API-first architecture | Integrates in hours, not months |

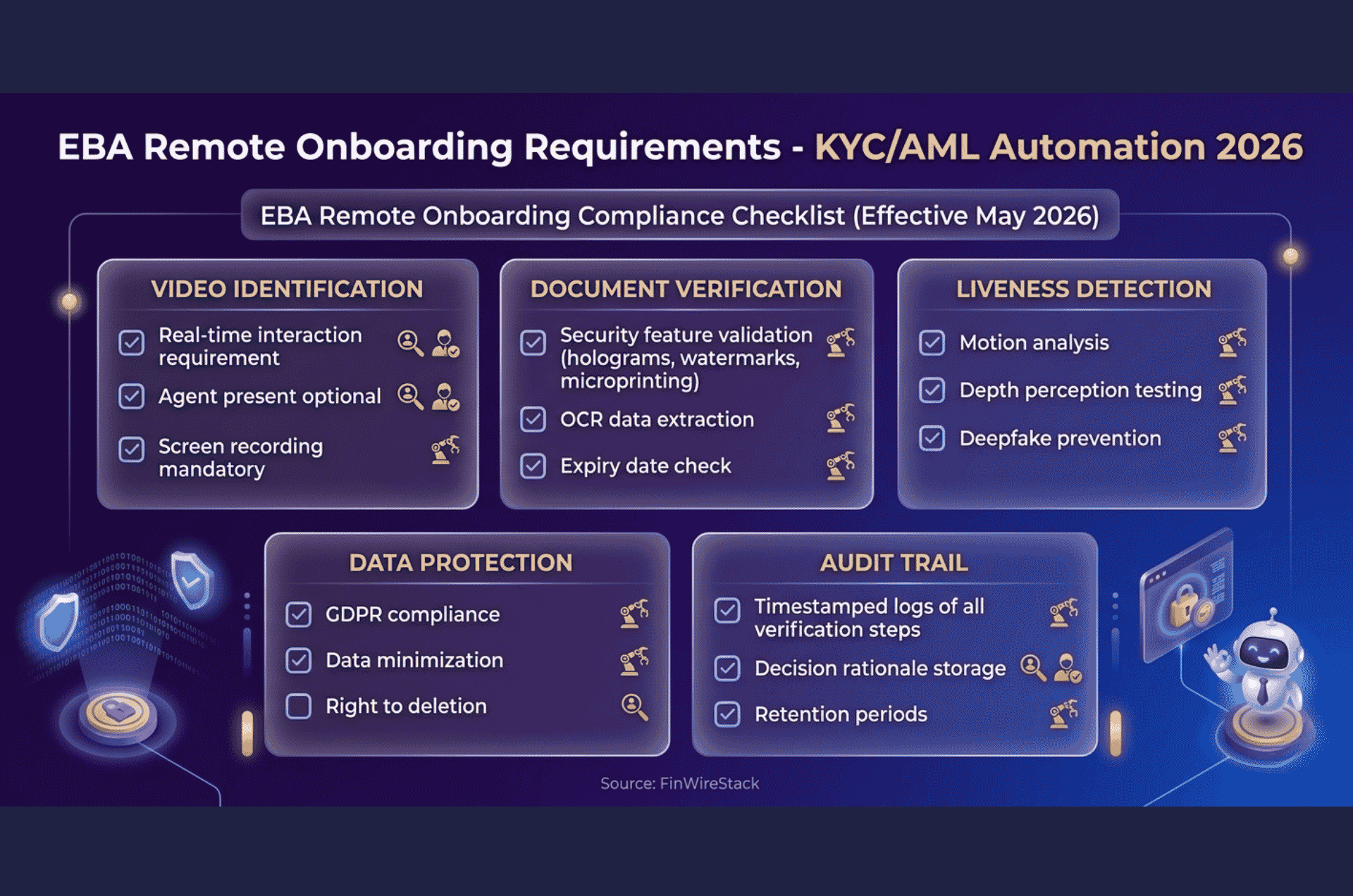

The EBA’s new Guidelines on remote customer onboarding specifically require the following:

| EBA Requirement | Automation Feature Needed |

|---|---|

| Video identification with live agent | Optional human review workflow |

| Document security features verification | AI-powered document authenticity checks |

| Liveness detection | Biometric liveness + motion analysis |

| Data protection compliance | GDPR/CCPA-compliant data handling |

| Audit trail retention | Complete timestamped logs |

KYC/AML automation for fintech startups must address each EBA requirement to serve European customers.

After evaluating 15 platforms specifically for fintech startups, here are the top 5 KYC/AML automation solutions for fintech startups.

Best for: Startups needing flexible, no-code KYC/AML automation

Persona offers a drag-and-drop workflow builder that requires no engineering resources. The platform handles identity verification, watchlist screening, and ongoing monitoring.

| Feature | Detail |

|---|---|

| ID document support | 200+ countries, 3,500+ document types |

| Verification methods | Document, biometric, database, knowledge-based |

| Watchlist sources | 1,000+ global sanctions, PEP, adverse media |

| Integration time | Hours (no-code) to days (API) |

| Pricing | Usage-based (0.50−3.00 per verification) |

Pros:

Cons:

KYC/AML automation for fintech startups with Persona starts at the lowest implementation barrier.

Affiliate Link: Try Persona (We earn a commission if you purchase through this link.)

Best for: Startups with international customers and crypto exposure

Sumsub provides all-in-one KYC/AML automation for fintech startups, including KYC, KYB, AML, and transaction monitoring. The platform has strong blockchain analytics for crypto transactions.

| Feature | Detail |

|---|---|

| ID document support | 220+ countries, 6,000+ document types |

| Blockchain analytics | Yes, for crypto and DeFi transactions |

| KYB (business verification) | Yes, including ultimate beneficial owners |

| Transaction monitoring | Included |

| Pricing | Custom (typical $1-3 per verification) |

Pros:

Cons:

KYC/AML automation for fintech startups with Sumsub works best for regulated and crypto-native companies.

Affiliate Link: Try Sumsub (We earn a commission if you purchase through this link.)

Best for: Startups prioritizing document verification accuracy

Onfido uses AI-powered document verification with industry-leading accuracy rates. The platform is trusted by major banks and fintechs globally.

| Feature | Detail |

|---|---|

| ID document support | 150+ countries |

| Verification accuracy | 99.5%+ |

| Liveness detection | Yes (motion-based) |

| Watchlist screening | Yes (via third-party integrations) |

| Pricing | 0.50−2.00 per verification |

Pros:

Cons:

KYC/AML automation for fintech startups with Onfido is ideal for document-heavy verification needs.

Affiliate Link: Try Onfido (We earn a commission if you purchase through this link.)

Best for: Startups needing best-in-class watchlist screening and transaction monitoring

ComplyAdvantage specializes in AML data. Their watchlist database covers 1,000+ sanctions lists, 10,000+ PEPs, and 300,000+ adverse media sources.

| Feature | Detail |

|---|---|

| Watchlist sources | 1,000+ sanctions lists, global coverage |

| PEP coverage | 10,000+ politically exposed persons |

| Adverse media | 300,000+ sources |

| Transaction monitoring | Yes, real-time |

| Pricing | Transaction-based (custom) |

Pros:

Cons:

KYC/AML automation for fintech startups with ComplyAdvantage prioritizes AML over identity.

Affiliate Link: Try ComplyAdvantage (We earn a commission if you purchase through this link.)

Best for: Startups needing high-conversion, user-friendly identity verification

Veriff focuses on the user experience of KYC/AML automation for fintech startups, with conversion rates exceeding 95% and verification times under 30 seconds.

| Feature | Detail |

|---|---|

| ID document support | 200+ countries |

| Average verification time | 15-30 seconds |

| Conversion rate | 95%+ |

| Liveness detection | Yes (passive + active) |

| Pricing | 0.80−3.00 per verification |

Pros:

Cons:

KYC/AML automation for fintech startups with Veriff prioritizes user experience and conversion.

Affiliate Link: Try Veriff (We earn a commission if you purchase through this link.)

KYC/AML automation for fintech startups requires matching platform strengths to your specific needs.

KYC/AML automation for fintech startups can be implemented rapidly using this 30-day plan.

| Day | Task | Time |

|---|---|---|

| 1-2 | Document your compliance requirements (geography, customer types, volume) | 4 hours |

| 3-4 | Evaluate 3-5 platforms using the comparison table above | 6 hours |

| 5-7 | Sign contract with chosen vendor and request sandbox access | 2 hours |

| Day | Task | Time |

|---|---|---|

| 8-9 | Set up API keys and configure webhook endpoints | 4 hours |

| 10-11 | Build customer onboarding flow around verification steps | 8 hours |

| 12-14 | Configure watchlist screening rules and risk thresholds | 6 hours |

| Day | Task | Time |

|---|---|---|

| 15-16 | Run 50-100 test verifications (use internal team) | 4 hours |

| 17-18 | Tune false positive/negative rates based on test results | 4 hours |

| 19-21 | Set up case management dashboard for manual reviews | 4 hours |

| Day | Task | Time |

|---|---|---|

| 22-23 | Train customer support team on verification flows | 4 hours |

| 24-25 | Soft launch to 5% of users, monitor error rates | 4 hours |

| 26-28 | Ramp to 100% of users | 2 hours |

| 29-30 | Set up ongoing monitoring dashboard and alerts | 2 hours |

KYC/AML automation for fintech startups can go from zero to production in one month.

For automated transaction monitoring approaches, see Agentic AI Fraud Detection for Community Banks.

Several critical regulatory changes took effect in May 2026 that directly impact KYC/AML automation for fintech startups.

The European Banking Authority’s new guidelines on the use of Remote Customer Onboarding Solutions became effective in May 2026 . Key requirements include:

| Requirement | Implication for Automation |

|---|---|

| Video identification must verify document security features | AI must detect holograms, watermarks, and microprinting |

| Liveness detection must prevent deepfake attacks | Multi-frame motion analysis required |

| Data processing must comply with GDPR | Automated data minimization and retention policies |

| Audit trail must capture all verification steps | Complete timestamped logs of every decision |

KYC/AML automation for fintech startups must incorporate these EBA requirements for European customers.

The Sixth Anti-Money Laundering Directive (AMLD6) is being implemented across EU member states in May-June 2026 . Changes include:

| Change | Impact |

|---|---|

| Expanded criminal liability | Compliance officers personally liable for AML failures |

| Cross-border access to beneficial ownership registries | Unified database of ultimate beneficial owners |

| New predicate offenses | Cybercrime and environmental crime added |

The SEC’s new Rule 13f-2 took effect in May 2026, requiring institutional investment managers to report large short positions. While primarily impacting investment firms, fintechs with lending or trading operations should monitor compliance.

KYC/AML automation for fintech startups must adapt to these changing regulatory requirements.

KYC/AML automation uses AI and APIs to automatically verify customer identities, screen against global watchlists, monitor transactions, and file regulatory reports—replacing manual compliance processes.

| Volume | Typical Cost per Verification | Monthly Cost (5,000 verifications) |

|---|---|---|

| Low (1,000-10,000/month) | 2.00−5.00 | 10,000−25,000 |

| Medium (10,000-100,000/month) | 1.00−2.00 | 10,000−20,000 |

| High (100,000+/month) | 0.50−1.00 | 5,000−10,000 |

Yes, the leading platforms (Persona, Sumsub, Onfido, and Veriff) have updated their solutions to meet EBA requirements for remote onboarding, including liveness detection, document security verification, and audit trails.

Sumsub offers blockchain analytics for crypto transaction monitoring. Other platforms may require integration with specialized crypto AML providers like Chainalysis or Elliptic.

Most fintech startups implement KYC/AML automation for fintech startups in 2-4 weeks using the 30-day plan above. No-code platforms like Persona can be live in days.

KYC/AML automation for fintech startups reduces but does not eliminate risk. Regulators expect reasonable efforts, not perfection. Maintain an audit trail showing your automated checks and any manual reviews performed.

For ongoing compliance management, see Fintech Compliance 101: What Small Businesses Need to Know.

KYC/AML automation for fintech startups is the single most important investment you can make in 2026.

| Platform | Best For | Starting Price |

|---|---|---|

| Persona | No-code workflows, fastest implementation | $0.50/verification |

| Sumsub | All-in-one + crypto, regulated fintechs | $1-3/verification |

| Onfido | Document verification accuracy | $0.50-2/verification |

| ComplyAdvantage | AML data depth, transaction monitoring | Custom |

| Veriff | Conversion rates, user experience | $0.80-3/verification |

| Don’t | Do |

|---|---|

| Wait for regulatory pressure to act | Implement automation before you need it |

| Hire 10 compliance officers | Automate first; hire exceptions |

| Build your own verification system | Use specialized vendors |

| Ignore EBA remote onboarding guidelines | Ensure your vendor is compliant |

| Treat compliance as a one-time project | Monitor continuously |

KYC/AML automation for fintech startups saves money, time, and regulatory headaches. The technology is mature, affordable, and proven. The only question is whether you will adopt it before or after a costly compliance failure.

Ready to automate your compliance? Compare KYC/AML automation platforms or download our vendor selection checklist.

You must be logged in to post a comment.

[…] For protecting your data, see KYC/AML Automation for Fintech Startups. […]